The Best Intentions...

A PACE Series — Article 2 Everyday Elders · Ars Moriendi Project

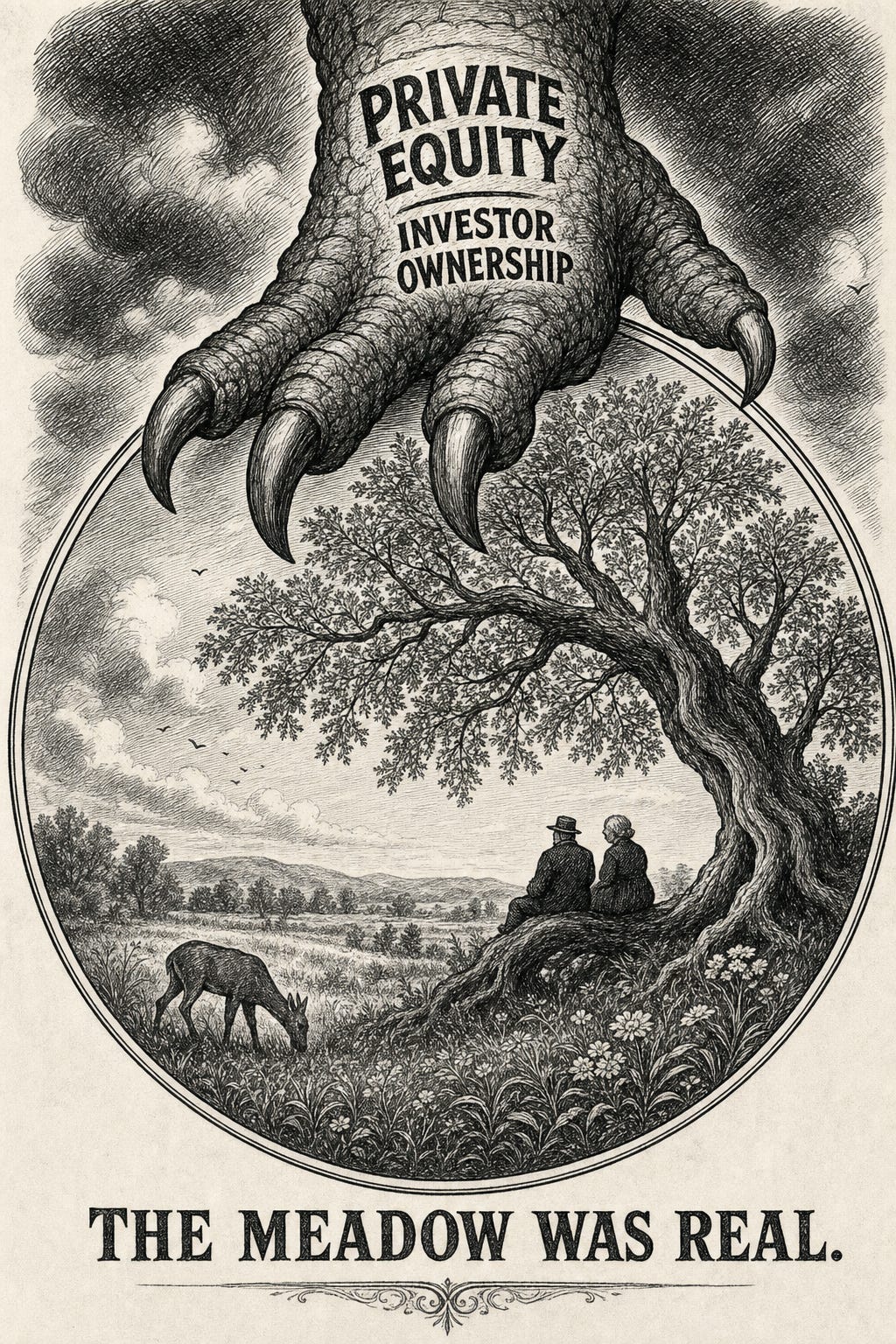

There was a crudely animated short film released in 1969, about ninety seconds long, called Bambi Meets Godzilla. For almost all of it, Bambi stands in a meadow while pastoral music plays. Then, without warning, a giant reptilian foot drops from above and crushes her. The joke works because the meadow is real. So is the violence.

For nearly half a century, PACE was the meadow.

That is not sentimental overstatement. The Program of All-Inclusive Care for the Elderly was built on a proposition so humane and so structurally unusual in American health care that it can still sound improbable when described plainly: take people old enough and frail enough to qualify for nursing-home care, and give them a coordinated team, a day center, transportation, medical care, therapy, and social support robust enough to keep them at home. Pay the program a fixed monthly amount. Let the doctors, nurses, social workers, aides, and therapists use that money to keep people well rather than to bill for each discrete episode of decline. And — by federal law, from the model’s earliest days until 2016 — entrust this work only to nonprofit organizations. PACE grew out of On Lok in San Francisco’s Chinatown, and, like On Lok, every PACE program in the country was, for nearly its entire history, a community-rooted nonprofit.

The design carried inherent danger from the beginning, but its founders and early federal stewards understood it. A capitated program — one that pays a fixed monthly sum per enrollee, regardless of services delivered — can reward mercy, thrift, vigilance, and common sense. It can also reward withholding, delay, and euphemism. That is why the original PACE model was so carefully constrained. The nonprofit-only rule was not decorative. It was part of the machinery.

For years, that machinery held. PACE remained a small, nonprofit world, local and unglamorous, reliant on trust and difficult to scale. It did not promise the kind of returns that excite modern finance. That was one reason it was largely left alone.

Then, in the middle of the 2010s, Washington began to ask a different question. Could PACE be expanded more quickly? Could it be modernized, loosened, made more flexible, more investable, and more accessible to new kinds of operators? Framed one way, these were practical questions about access and growth. Framed another, they were the first tremors beneath the meadow.

The year everything was supposed to change was 2016. Not by itself, and not in a vacuum — the policy mood had been shifting since at least May 2015, when the Department of Health and Human Services delivered a report to Congress on a long-running for-profit PACE demonstration and concluded that for-profit operators had performed comparably to nonprofits in quality, access, and cost. That report became the regulatory ignition switch. On August 16, 2016, the Centers for Medicare & Medicaid Services published a proposed rule — CMS-4168-P — to update the PACE program for the first time in a decade, lifting the nonprofit-only restriction and opening the program to investor-backed operators. CMS framed the change in terms of access and modernization. Flexibility became a term of art. Modernization became a promise. Scale became a public good in itself. The old nonprofit restrictions, once treated as prudent safeguards for a vulnerable population, began to look to some policymakers and operators like friction.

This was not, on its face, an absurd conversation. PACE had remained relatively small, and many eligible elders still lacked access to it. Advocates of expansion could reasonably argue that a successful model should not remain boutique simply because its founders had been cautious. In health policy, as in other fields, noble aspirations are often accompanied by sincere frustration that a good thing has not spread faster.

But speed changes a program’s moral chemistry. So does ownership.

The proposed rule from August 2016 would not be finalized until 2019, but the door was already open. While CMS was drafting language on flexibility and modernization, the private-equity firm Welsh, Carson, Anderson & Stowe was, in the same spring of 2016, finalizing a majority investment in a Denver-based PACE operator, InnovAge. What had once been a tightly bounded demonstration model was about to be treated as a platform that could accommodate a wider range of operators and operational strategies.

That shift might still have remained abstract to the general public if not for a single company.

InnovAge, headquartered in Denver, became the country’s largest PACE provider. It was also something PACE had not originally been designed to accommodate: a large, investor-backed company organized for growth. Welsh, Carson, Anderson & Stowe acquired a majority stake in InnovAge in May 2016. Apax Partners later acquired a major stake through a 2020 equity recapitalization. In March 2021, InnovAge went public on the NASDAQ at $21 a share, raising roughly $350 million in its initial public offering.

On paper, this could be told as an American success story. A once-local elder-care model had matured into a scalable enterprise. Capital had arrived, and public markets had opened. Institutional investors were signaling confidence that a program once considered too specialized and too relational to attract serious money could, in fact, become a growth business.

That was the promise, not the whole story.

The deeper problem was not simply that investors had arrived. It was that investor logic and PACE logic were never quite the same. PACE is built on the claim that a frail elder is safest when the program surrounding her can afford to spend what is necessary before a crisis rather than after it. Private equity and public markets ask a different set of questions. How quickly can enrollment grow? What margins are available? Where are labor costs low enough to compress? Which operational constraints can be labeled inefficiencies? How much of the future can be pulled forward and recognized now?

None of those questions is illegal. None sounds especially theatrical in a boardroom. But each shifts the center of gravity away from the elder and toward the enterprise. In a program where every unspent dollar can also, from another vantage point, appear as retained gain, that shift is not incidental. It is the story.

And in 2021, for a moment, it seemed likely to be the year that story would finally be confronted.

InnovAge’s IPO came with the bright rhetoric that accompanies nearly all IPOs: confidence, addressable markets, growth strategy, and managerial discipline. Around the same time, federal oversight was intensifying. Investigations, sanctions, and public reporting made it harder to sustain the fiction that scale and investor discipline were merely neutral tools dropped into a morally self-correcting system. They were pressures. They changed behavior. In the wrong environment, they could also change what the program was for.

That matters because PACE had always rested on a quiet bargain with the public. Families would accept a closed network, a single integrated program, and a monthly payment stream flowing in whether or not every possible service was visibly rendered, because the organization receiving that money was supposed to be structurally constrained from siphoning off the difference. Remove or weaken that constraint, and the bargain changes, even before a single scandal breaks.

In retrospect, this was the real significance of the 2016 shift. The opening of PACE to investor-backed ownership was not merely a policy tweak. It was a philosophical revision. It asked the public to believe that the same payment model that worked as a moral instrument within a nonprofit framework would work just as well once financial actors were given a legitimate claim on the surplus.

Sometimes a policy transformation announces itself with speeches and banners. More often, it arrives in administrative language: flexibility, innovation, modernization, access. The words are not false. They are incomplete. What they leave out is the older wisdom that some programs survive precisely because their inefficiencies are moral safeguards, and that some forms of slowness create the climate that protects the people inside them.

In California, where PACE had some of its deepest roots, the emerging conflict would soon become impossible to ignore. Questions about expansion, oversight, market entry, quality, and who exactly was profiting from this model were no longer theoretical. They became administrative and political. They became local. They became urgent.

The tragedy of this moment is that the reformers were not always wrong about the problem. More elders needed access. More counties needed programs. The nonprofit world was not magically immune to failure, complacency, or mediocrity. But when policymakers reached for scale, they also loosened the guardrails that had made the model trustworthy in the first place.

That is how a meadow changes. Not all at once, and not always by visible invasion. Sometimes the climate around it shifts — the air dries, the seasons lengthen, the shadows lean a little farther across the grass — and what once grew easily begins to grow only with effort. The change arrives in increments, narrated by people speaking the language of improvement. And sometimes Godzilla crushes it.

The question that now hangs over PACE is not whether the original promise was real. It was real. The question is whether a program designed to keep frail elders from being treated as units of revenue can survive once revenue-minded owners are invited inside — and once the climate around the program has been altered to make their presence feel natural.

InnovAge would become the clearest test of that question. California would become one of the places where the consequences could no longer be ignored. And what looked, in policy memos and investor decks, like modernization would begin to look to others like something simpler and older: extraction.

The next article in this series will follow the money and the structure more closely, beginning with InnovAge and the problem of what capitation becomes when the fence is no longer load-bearing.

· · ·

Rick Beeman is the author of Bought for Parts: How Wall Street is Profiteering on Your Mother’s Pain (April 2026) and President of Ars Moriendi Project, a California 501(c)(3) public charity working on accountability in long-term care.

Everyday Elders is a publication of Ars Moriendi Project.

Sources

• CMS, “Programs of All-Inclusive Care for the Elderly (PACE) (CMS-4168-P),” proposed rule fact sheet, August 11, 2016. https://www.cms.gov/newsroom/fact-sheets/programs-all-inclusive-care-elderly-pace-cms-4168-p

• Federal Register, “Medicare and Medicaid Programs; Programs of All-Inclusive Care for the Elderly (PACE),” 81 FR 55492, August 16, 2016. https://www.govinfo.gov/content/pkg/FR-2016-08-16/html/2016-19153.htm

• CMS, “PACE Final Rule (CMS-4168-F) Fact Sheet,” May 2019. https://www.cms.gov/newsroom/fact-sheets/programs-all-inclusive-care-elderly-pace-final-rule-cms-4168-f

• Welsh, Carson, Anderson & Stowe, InnovAge investment profile. https://wcas.com/firm/investments/innovage/

• Apax Partners, InnovAge partnership profile. https://www.apax.com/partnerships/innovage/

• IPOScoop, “InnovAge Holding Corp.” IPO record (priced March 3, 2021). https://www.iposcoop.com/ipo/innovage-holding-corp/

• NORC at the University of Chicago, “PACE Market Assessment: For-Profit Expansion and Growth,” March 17, 2025. https://www.norc.org/content/dam/norc-org/pdf2025/PACE%20Market%20Assessment_For-Profit%20Expansion%20and%20Growth_Final%20Report%203.17.2025.pdf

• Bowblis JR et al., “Growth of the Program of All-Inclusive Care for the Elderly,” JAMA Health Forum, 2025. https://pmc.ncbi.nlm.nih.gov/articles/PMC11736723/

• Bambi Meets Godzilla (Marv Newland, 1969). https://www.imdb.com/title/tt0064064/